The credit score to buy a house can be as low as 580. A low credit score doesn't have to lock you out of home ownership. A mortgage will probably cost you more (both in dollars and angst) than someone with stellar credit, but many lenders are willing to work with you. Here's what you need to know about low-credit score mortgages:First, let's debunk the home-buying myth that you have to have a gold-plated credit score to buy a house. Lenders review your whole financial picture. If you have a steady income, a regular payment history, and some cash in hand, that will help balance your less-than-perfect credit.Here's how FICO generally categorizes credit scores:

- 800+ = Excellent credit score

- 740-799 = Very good credit score

- 670-739 = Good credit score

- 580-699 = Fair credit score

- Below 580 = Poor credit score

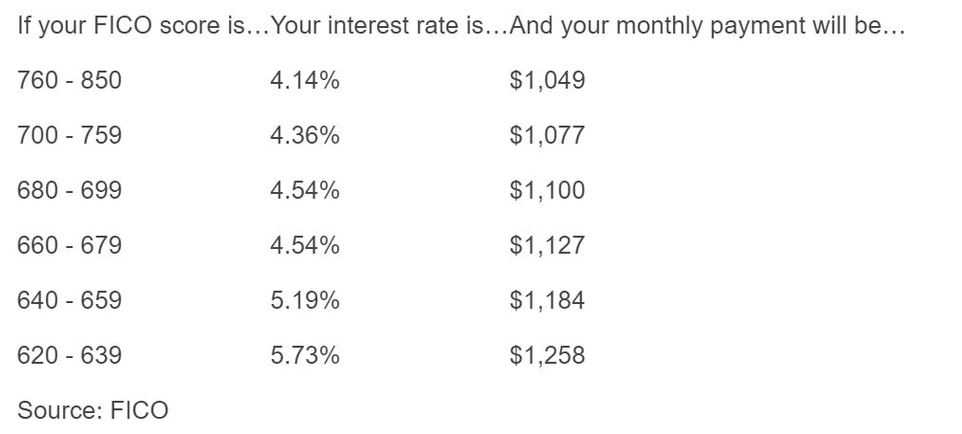

A credit score of 669 or below typically makes you a "subprime" borrower, according to FICO. That means you're a bigger risk, so loans will cost more, and your options will be limited.Your primary low-credit-score mortgage option will be FHA , which sometimes give loans with credit scores as low as 580. But the lower your score, the more it will cost you.How Does Your Credit Score Affect Interest Rates?You may pay more in the form of a larger down payment, a higher interest rate, private mortgage insurance, or points, which are fees attached to the loan.How much more interest might you pay? Let's say you're going for a $216,000, 30-year, fixed-rate mortgage. Here's how your rate could change based on your score. (FYI, the monthly payment estimate includes only interest and your principal, not insurance, taxes, private mortgage insurance, or other expenses.) Rates here may not reflect current conditions. So... Buy Now Or Work On My Credit?That's a good question and one only you can answer. If your rent is astronomical, it might be better to own sooner and refinance when your credit improves. For others, it may be smart to }improve your credit first. A lender can help you decide. Or you can use an online tool to estimate the cost of different scenarios.If you're going to apply for a low-credit-score mortgage, more cash in the form of a bigger down payment helps. Plus, it can reduce your interest rate, which reduces your monthly payment."My recommendation for any client would be wait and save toward a bigger down payment," says Melissa Finnell, regional mortgage manager with the bank BB&T. "A lower loan-to-value ratio offsets a higher interest rate, and this gives clients time for their credit to rehabilitate, too."How Do I Boost My Credit Score?If you opt to work on your credit before getting a mortgage, here are a few ways to do it:

So... Buy Now Or Work On My Credit?That's a good question and one only you can answer. If your rent is astronomical, it might be better to own sooner and refinance when your credit improves. For others, it may be smart to }improve your credit first. A lender can help you decide. Or you can use an online tool to estimate the cost of different scenarios.If you're going to apply for a low-credit-score mortgage, more cash in the form of a bigger down payment helps. Plus, it can reduce your interest rate, which reduces your monthly payment."My recommendation for any client would be wait and save toward a bigger down payment," says Melissa Finnell, regional mortgage manager with the bank BB&T. "A lower loan-to-value ratio offsets a higher interest rate, and this gives clients time for their credit to rehabilitate, too."How Do I Boost My Credit Score?If you opt to work on your credit before getting a mortgage, here are a few ways to do it: